The Indian Government’s latest initiative-the Central Bank Digital Currency (CBDC)-will help solve the various payment impediments that are routinely faced by marketers and businesses while keeping track of all the financial transactions and providing a system to manage them. The digital rupee or e-rupee has been rolled out for wholesale marketers from November 1. Experts believe it to be a new page in the annals of the Indian banking system and a milestone moment towards a paperless economy.

As she presented the Budget 2022, Finance Minister Nirmala Sitharaman emphasised on the importance of the e-rupee and said that it will be issued by the Reserve Bank of India (RBI). The digital rupee will be introduced using technologies such as blockchain.

“The Central Bank Digital Currency will give a big boost to the digital economy. Digital currency will also lead to a more efficient and cheaper currency management system,” said Sitharaman.

Also Read: Budget 2023-24: Pre-budget meetings conclude with suggestions on ‘Green’ MSMEs, custom duties & more

What makes the digital rupee so important, what are the differences between Wholesale CBDC and Retail CBDC and what are the benefits that the e-rupee offers?

What is the CBDC?

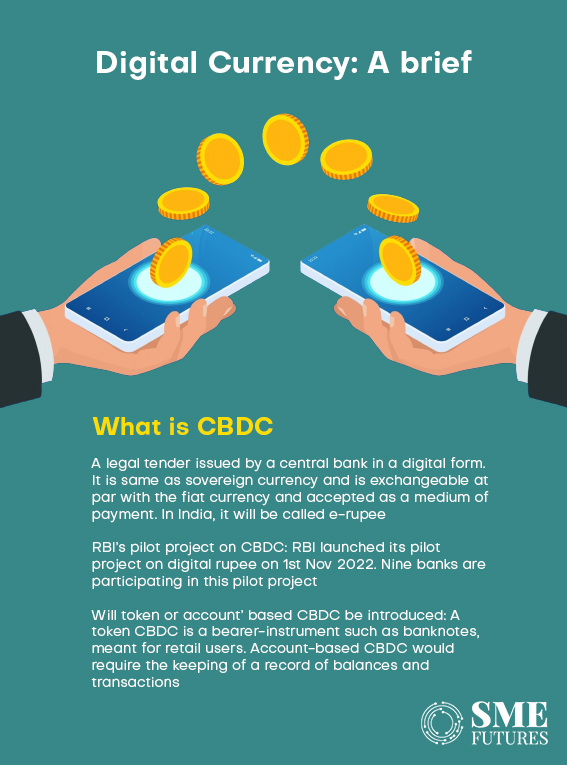

The Central Bank Digital Currency (CBDC) is a digital note currency, which means that it is a digital currency note that is issued by the central bank. Countries across the globe are working on making digital currency an acceptable mode of payment. Digital currency helps in facilitating the current payment systems of physical notes. It is easy to handle and manage.

“Digital currency is expected to transform the settlement systems for transactions and make them even more feasible for the users. The CBDC will also speed up cross-border transactions, even for the users who are not linked to a particular bank account,” says Rachit Chawla, Founder & CEO, Finway FSC.

Wholesale CBDC vs Retail CBDC

Based on its use and function, CBDC can be broadly divided into two types, Wholesale CBDC and Retail CBDC.

Wholesale CBDC is to be used to make interbank payments more efficient while Retail CBDC will be owned and used by individuals, be it the private sector or businesses or the non-financial consumers.

Wholesale CBDC is designed for financial institutions where it enjoys restricted access. In Retail CBDC, we can transfer money from one individual to another, making it accessible to everyone.

Wholesale CBDC can be efficiently adopted in countries with advanced economies. Retail CBDC can function smoothly in a country with an emerging economy.

Also Read: FM asks startups to focus on climate change solutions

“The digital currencies have the potential to transform the settlement systems for transactions and make them more efficient and secured; thereby bolstering the digital economy and bringing in financial inclusion. Wholesale CBDC is expected to bring in more transparency because of the application of blockchain technology,” Chawla points out.

Be it Wholesale or Retail CBDC, both aim to bolster India’s economy by taking its payment systems to the digital level. The government can keep an account of the transactions taking place and also limit the dependability on physical currency notes.

“The digital ledger that these currencies use to process and record transactions could help prevent banking fraud. Retail CBDCs would be issued to the general public and will serve as a public digital banking option, which can be owned in a wallet or in an account and can be used for payments,” says Musharraf Hussain, COO, Ezeepay.

Crypto currency vs CBDC

Crypto currency is something that we have all heard about. Crypto currency runs on blockchain which can be described as a distributed public ledger. Crypto currency is still an emerging market in terms of financial use and for other extensive uses as well. Many experts believe it to be the future of money and that is where the CBDC comes in.

Also Read: 3-minute slot, a “Cheap Joke”: Ten trade unions boycott pre-budget meeting

While crypto currencies have no issuing body or any kind of regulating body to keep a check on the transactions, the CBDC is regulated by RBI. It acts as an authority by keeping checks and balances on the use of digital money or the CBDC.

Another point to keep in mind is that to use the CBDC, customers don’t need an account or a wallet, like in the Unified Payment Systems (UPI), where a user’s mobile number and Aadhar card act as a means of verification and are linked through their bank account. To use crypto currencies, users need a crypto wallet that has a wallet address or public key which are essential to complete transactions. A crypto wallet is an application that allows users to manage their crypto coins and store their crypto currency keys.

How can the CBDC revolutionise India’s economy?

Many countries are exploring the benefits of the CBDC. While some are still testing and researching about it to find ways to fit it according to their country’s economies and policy systems, some are already in the distribution phase.

Bahamas has its own CBDC called Sand Dollar. The local CBDC has been in circulation for more than a year now.

Also Read: Uncertain yarn prices: Powerlooms to remain shut in Tiruppur, Coimbatore

In China, the digital currency is called e-CNY. Their local CBDC is showing humungous progress with about a hundred million users and transactions worth billions of yuan.

Sweden too is working on its own CBDC. Sveriges Riksbank, the central bank of Sweden, has been mulling about the CBDC. They’ve made a proof of concept and are now testing the policy and technology implications of the CBDC.

To understand the CBDC and its implications, it is necessary to know three crucial points:

- Each country’s economy is different and hence, the implications of the CBDC will be different for every country i.e., there is no universal use case for the CBDC; it depends on the economy of a particular country.

- Financial stability and privacy should go hand-in-hand when adopting the CBDC for a country.

- A country’s policy and a change in design of the CBDC should always maintain a balance. It is necessary to keep a check on both the fronts.

In India, nine banks will participate in Wholesale CBDC’s pilot project. These banks include YES Bank, HSBC, the State Bank of India, HDFC Bank, ICICI Bank, IDFC Bank, the Bank of Baroda, Kotak Mahindra Bank and the IDFC First Bank.

“The 9 banks selected as Wholesale CBDCs will seek to settle interbank transactions on the CBDC framework. The framework will attempt to reduce transaction costs by reducing or replacing the need for a settlement guarantee infrastructure or for a collateral to mitigate settlement risk. This framework could also help reduce costs in settling cross-border transactions. The Stellar blockchain is built on solving these use cases, especially for small ticket remittances for illiquid currency pairs between banks,” says Anirudh A. Damani, Founder, Artha Group.

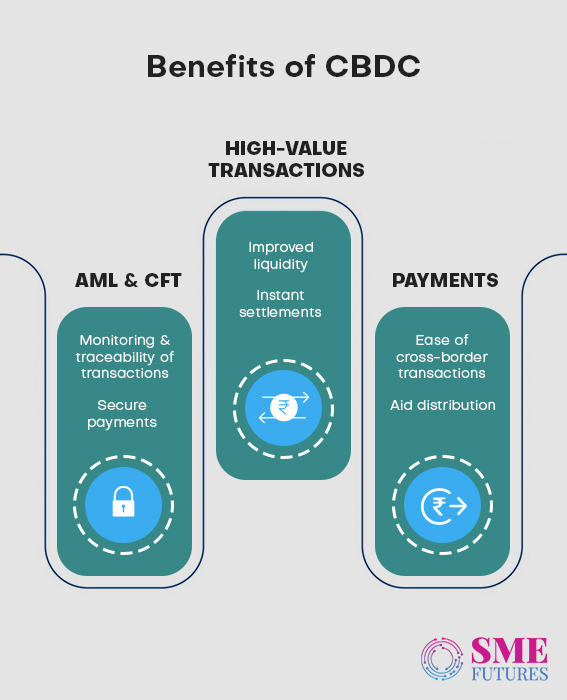

Benefits of the CBDC

According to a Bank for International Settlements (BIS) report, wholesale CBDCs are intended for the settlement of interbank transfers and related wholesale transactions. They serve the same purpose as the reserves held at the central bank but with additional functionality.

Also Read: Indian musical instruments exports increased 3.5 times in 8 years

Furthermore, settlement systems can be revolutionized with the application of the CBDC for financial transactions that are undertaken by banks in the interbank market, the capital market and even by the banks dealing with the government securities segment by making them more safe, secure and efficient in terms of operational costs, collateral use and management of liquidity.

Another benefit of the CBDC is that it will reduce the costs associated with the management of physical currency notes. The E-rupee will also go a long way in saving the costs associated with the printing, storing and distribution of currency notes in banks. Thus, it will help in saving the environment by reducing paper usage.

It will also facilitate cross-border transactions, make cash management seamless and operations smoother.

“Three significant issues are posed by the advent of CBDCs: a rise in privacy threats, selecting privacy and security enhancing technologies, and regulatory architecture. The increased risk to users’ privacy is the first issue to be addressed with CBDCs. To stop data breaches, reliable data security systems must be installed. The Data Protection Bill and the establishment of the Data Protection Authority to monitor privacy compliance are still pending in India,” Arun Singhal, Founder, Source.One points out.

The way forward

“The primary focus of the RBI would be to assure financial inclusion, lower fraud and money laundering, ensure sovereign alternatives for digital payments, encourage local payment innovations, and develop a new vehicle for our monetary policy. These are just a few systemic objectives that central banks can address using CBDCs. In addition, it will be the basis for financial and economic stability, for ensuring competition and for promoting efficiency in payment markets,” Musharraf Hussain, COO, Ezeepay points out.

The quick adoption of the CBDC in real time depends hugely on the infrastructure that will be used for trading and for smooth exchanges. For this, Retail CBDC has to be integrated with the Real Time Gross Settlement (RTGS).

Also Read: Rupee weakening due to dollar strengthening, economy can’t be blamed: Goyal

Digital currency is a huge step in India’s journey towards a cashless economy. The need of the hour is to make people more aware about its advantages and to promote its usage among the common people.

“A big challenge facing the CBDC is getting the POS terminals to accept an additional form of currency. It would require businesses and consumers to open digital wallets that can store currencies. Users will have to accept the direct control that the government would have on these wallets. Whether users would allow their entire monetary wealth to be converted into digital cash or whether it would be a complementary feature with niche use cases could be the existential questions facing CBDCs,” says Damani.

The RBI has said that the digital rupee system will “bolster India’s digital economy, enhance financial inclusion and make the monetary and payment systems more efficient”. The digital rupee has ushered in a new era, and it will go a long way in boosting the payment systems of the country.