As the day of the unveiling of the Union Budget 2023-24, i.e., February 1st, approaches, industry stakeholders are on high alert. And India’s insurance industry is no exception. With a slew of announcements last year, the industry saw a steady increase in its growth. In addition, the Finance Ministry recently issued an announcement on the Insurance Laws (Amendment) Bill 2022, which proposes changes to the insurance policy framework. As a result, the industry’s stakeholders are optimistic about how this year’s budget announcements will affect the sector.

Here is their wish list.

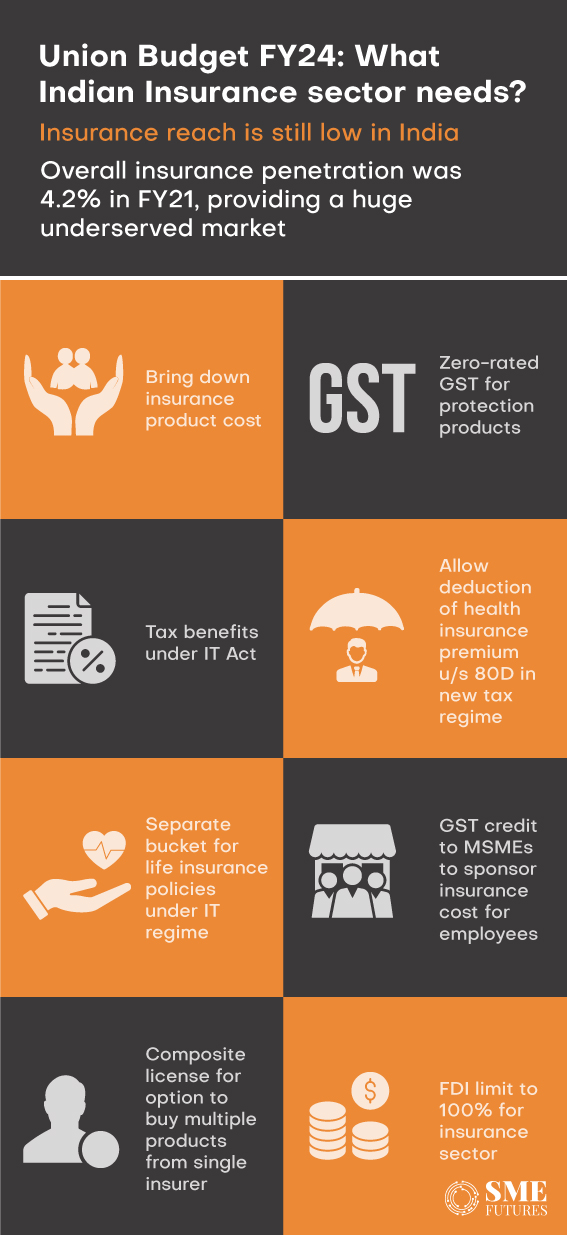

Bring down insurance costs

One of the sector’s main concerns is the country’s low insurance penetration. The stakeholders blame the high insurance costs for this.

Vighnesh Shahane, MD & CEO, Ageas Federal Life Insurance says that the insurance industry’s wish list has been largely the same for the last 4-5 years with the aim of driving insurance penetration in the country.

“To increase the penetration of pension and to make India a pension society, especially since we don’t have any social security cover, our request is to make pensions tax-free in the hands of the customer because the pension premium is already paid through taxable income. So, we recommend that the proceeds of the pension / annuity should be made tax-free in the hands of the customer or a deduction for the principal component should be allowed,” he says.

Alternatively, we could have a separate bucket for pensions in the range of Rs. 50,000-75,000- that would help to level the playing field with NPS, he adds.

“We recommend zero-rated GST for protection products as an 18 per cent GST makes the term plans costlier. To increase insurance penetration in the country, the basic protection plans should be made available under zero-rated GST,” he further suggests.

Cut down tax rates

To bring down the costs, Rakesh Jain, CEO, Reliance General Insurance, suggests cutting down the GST.

“In spite of the pandemic, the health insurance penetration in our country is very low. Due to this low coverage, the cost of insurance becomes high. To bring down its cost, the GST rate should be reduced to 5 per cent from the current 18 per cent,” he points out.

Also Read: Budget 2023: Agro-chem industry seeks cut in GST, import duty on crop protection chemicals

Currently, the health insurance premium paid to cover individual members is allowed a deduction ranging from Rs 25,000 to Rs 50,000. Jain urges that in view of inflation, the current limit of the maximum of Rs 50,000 should be increased to Rs 100,000 to induce people to buy adequate insurance covers, he further says.

“The benefit of a reduced tax rate of 10 per cent on long-term capital gain (LTCG) above Rs 1 Lac should also be extended to the insurance sector. Also, the premium paid for home insurance against the risk of various disasters should be given as a tax incentive by way of deduction under Chapter VI A to promote home insurance,” he elaborates.

According to Jain these steps will provide relief to the existing policyholders and will encourage our uninsured citizens to protect themselves with an insurance. Especially in the health insurance sector, it will encourage the Indian population to avail timely healthcare, thereby paving the way for a healthier country, which is vital for our nation’s long-term prosperity.

“The implementation of these tax benefits will also increase the affordability of insurance products and augment insurance penetration in the country, giving a much-needed boost to the insurance sector. Additionally, 5 per cent GST is charged on room rents exceeding Rs. 5,000 per day by clinical establishments. Insurance companies, while settling health insurance claims, are required to include this GST in the settlement amount. A clarification is required as to whether this GST is available as an Input Tax Credit to insurance companies,” he points out.

Benefits under income tax

Besides life savings, people mainly see insurance policies as tax saving assets. Hence, stakeholders are urging the government to allow insurance tax benefits under the new tax regime as well.

“The deduction of the health insurance premium u/s 80D should also be allowed under the new tax regime,” says Jain.

Shahane of Ageas also adds in, saying, “The current limit of a health premium (including preventive medical check-up costs) under Section 80D is only Rs. 25,000 and needs to be increased. The last two years of COVID-19 have proven that the current limit is not enough, and they need to significantly increase this limit. Because all said and done, people do buy life and health insurance for tax-saving purposes, so we do need to give them the benefits of a higher deduction limit.”

As per a budget announcement a couple of years ago, for ULIPs with an aggregated premium amount of Rs. 2.5 lakh pa or more, the maturity amount, which was earlier tax-free under Section 10(10D) of the Income Tax Act, became taxable. This should be reversed as it disincentivises big ticket investments, he suggests.

Section 80C of the Income Tax Act is currently cluttered with several investment options such as life insurance premium, PPF, ELSS, NSC, NPS, principal on home loan amongst others. If you are a salaried employee, most of it goes into EPF and PF.

Also Read: Why are financial advisors imperative for MSMEs?

“So, we would recommend a separate bucket for life insurance policies or an increase in the limit from Rs 1.5 lakh to Rs 2-2.5 lakh. At least a separate section for term policies would be helpful given the huge protection gap in the country,” adds Shahane.

Raising the TDS exemption limit on insurance commissions (u/s 194D of the IT Act) from the current level of Rs. 15,000 would provide a greater impetus to insurance agents.

Another suggestion comes from Abhay Tewari, Chief Executive Officer of SUD Life Insurance. He requests the government to waive the income tax on annuity incomes up to Rs 25,000 monthly for the age bracket of 60 years and above to enhance old age income security for all. He believes this should be over and above the current tax exemption on incomes up to Rs 5 lakh per annum. “This will boost the pension and life insurance sector and will help the government to mobilise the long-term funds that are required for infrastructure creation,” he elucidates.

Measures for businesses

In the upcoming budget, the government should look at offering GST credit to small and medium-sized businesses that sponsor the cost of insurance and wellness for their employees, says Yogesh Agarwal, Founder and CEO, Onsurity.

“This will further boost and motivate SME employers to provide adequate healthcare to their employees and in turn, reduce the burden on the government to provide the necessary healthcare to the country’s missing middle. Health and wellness have a direct impact on productivity and loyalty which in turn influences the country’s GDP,” he says.

A composite license is another aspect that the government can work on. The government should push for this because this will benefit the industry and the policyholders as well.

“It will give the insurers the necessary economies of scale and the customers the option to buy multiple products from the same insurer, lowering the cost of distribution (40- 50 per cent of the premium) in turn, which is one of the major costs of operating an insurance business. For policyholders, this will reduce the burden of excessive documentation and remembering renewal timelines,” Agarwal further says.

Other recommendations

The Insurance Regulator along with the government has taken some significant steps over the last year with the aim to enhance insurance penetration across the country. However, the stakeholders are looking forward to major changes this year and are hoping for the introduction of measures that can further spur this sector’s growth.

Anup Rau, MD & CEO, Future Generali India Insurance suggests increasing the FDI limit. “The much-awaited proposal to increase the FDI limit to 100 per cent in insurance could be taken up in the Union Budget ’23, which would augur well for insurers who will get fresh capital. With the uptick in healthcare costs, there is a strong case for increasing deduction limits for health insurance in the coming budget,” he says.

Talking about bonds and their role, Tewari of SUD Life Insurance suggests a few more measures regarding insurance bonds. “In keeping with the theme of overall infrastructure creation, the centre could look at offering deferred liability long-term bonds (up to 50 years). Life insurance companies will subscribe to it and support the government’s growth initiatives. Also, if the government considers issuing partly paid bonds, it will again help the economy in mobilising long term funds and the life insurance sector companies will subscribe to it for effective asset-liability management,” he further adds.

Also Read: As they ring in 2023, here’s how women entrepreneurs look back at 2022

Insurance companies are also hoping for industry consolidation to occur sooner rather than later. The distribution architecture proposed by the regulator, BIMA Sugam, will change the way in which consumers buy insurance in the Indian market.

With the changes that have been proposed in the Insurance Law and Regulation, an insurance company could very well become a ‘One Stop Shop’ for an Individual’s or corporate’s protection, retirement, and well-being needs. Meanwhile, experts claim that reinsurance rates are approaching pre-COVID levels in certain age brackets due to the normalisation of the overall claim experience over the last 8-12 months. As a result, the expectations from this budget are extremely high.