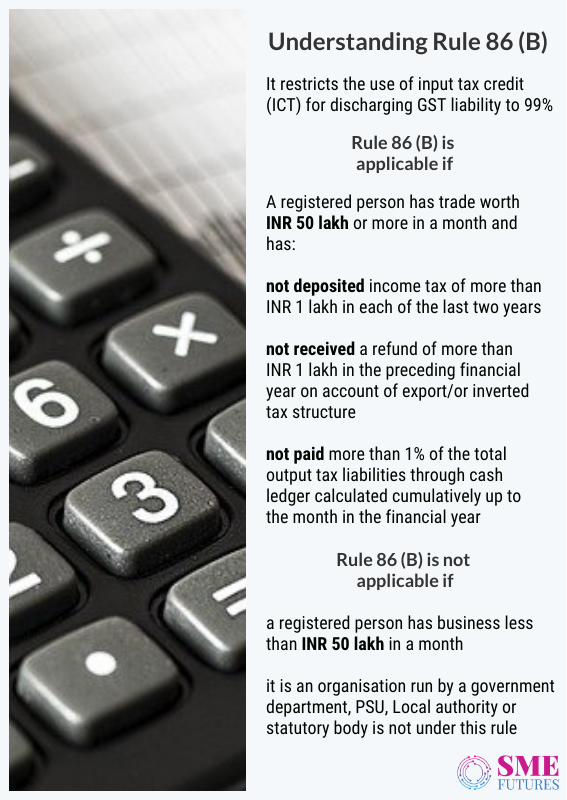

A government notification issued few days before the end of 2020 has caused a stir among traders. The notification is about the new GST amendments and tax-payers have numerous apprehensions about it. One of them is Rule 86B which came into force from 1st January 2021 and restricts the use of input tax credit (ICT) for discharging GST liability to 99 per cent.

This infers that from January 1 businesses whose monthly turnover is over Rs 50 lakh have to pay at least 1 per cent of their GST liability in cash as a mandate. “The registered person shall not use the amount available in electronic credit ledger to discharge his liability towards output tax in excess of 99 per cent of tax liability, in cases where the value of taxable supply … in a month exceeds Rs 50 lakh,” the Central Board of Indirect Taxes and Customs (CBIC) said.

The primary motive behind introducing stringent changes in the GST law is to curb practice of fake invoicing which Indian government is tackling since the launch of GST regime. A report by fifteenth finance commission that came out in early 2020 estimated that government might be losing five lakh crore, or about 40 per cent of GST collection target annually. This would account for a loss of around 2.4 per cent of the GDP nearly.

Just recently, GST authority in Delhi raided an illegal manufacturing unit for tax evasion of Rs 831.72 crore. In another three-week drive, the Directorate General of GST Intelligence (DGGI) has arrested 104 individuals in connection with 1,161 cases of tax credit fraud. As many as 3479 fake entities with GST registration were unearthed during the drive. Furthermore, the regular nationwide drive against submission of fake GST invoices has indicated enormity of GST frauds.

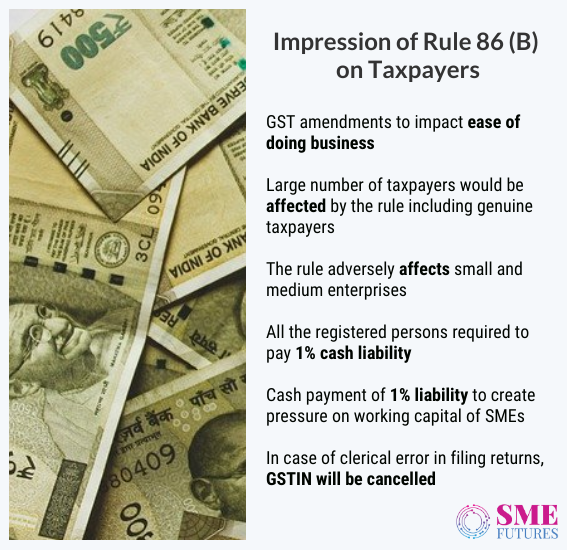

Meanwhile, businesses and Confederation of All India Traders (CAIT) has urged the government to scrap the rule with other demands calling it as ‘counterproductive.’ They are also of opinion that a huge section of taxpayers would be affected by this. According to them, the GST system is a much-complex taxation system that puts greater compliance burden on traders.

However, the government is in no mood to defer its decision despite receiving regular pleas from various trade’ associations. In fact, the CBIC has tried to clear air around the misconceptions on the amended GST rules in a series of tweets. Let us understand this law and see how it is going to impact various sections of tax-payers.

An explainer to rule 86B

The rule 86B has been a preferred topic of debate among accountants. The rule is embedded in CGST Rules 2017 and has an over-riding effect over other rules. The primary intent of rule is to block ITC and it is not applicable for every taxpayer. Rule 86B is applicable only if the export turnover is more than Rs 50 lakh in a month for an organisation.

Under this rule, if taxpayer has sufficient balance in its electronic credit ledger, the registered person cannot use the whole amount to discharge liability towards output tax in excess of 99 per cent. In addition to it, if a registered person supplies taxable supply (other than exempt supply, zero rated supply) in a month which is more than Rs 50 lakh then 1 per cent of such tax liability shall be paid in cash. For instance, if a firm supplies goods or service for Rs 70 lakh and tax on the product is 18 per cent, then the amount payable for taxable supply will be Rs 12,600.

“The limit is not to be checked with respect to preceding financial year but for each month for which return is being filed. Therefore, in cases where in turnover of taxable supply is less than Rs 50 lakh then this restriction would not be applicable. Suppose, if turnover exceeds in subsequent month then Rs 50 lakh, then restrictions would have to be checked,” explains Dr. Sanjiv Agarwal, CA and Managing Partner, Agarwal Sanjiv & Company on a blog.

On the other hand, the rule doesn’t apply on taxpayers in some scenarios. This includes the taxpayer itself, or specified persons such as the proprietor, karta, managing director, whole-time directors, or any of its two partners, and members of the managing committee of associations or board of trustees.

Also according to the case, people who have paid more than Rs 1 lakh as income tax under the Income-tax Act, 1961 in each of the last two financial years are also exempt from it. Secondly, a taxpayer when he or she has received a refund of unutilized ITC exceeding Rs 1 lakh in the preceding financial year on the account of either zero-rated outward supplies made without payment of tax, or inverted duty structure is also exempt from it.

Further, the taxpayer is also exempt from it when he or she has discharged GST liability by way of cash exceeding 1 per cent of the output tax liability, or has applied cumulatively up to the relevant tax period in the current financial year. This means that taxpayer has to keep a track on cumulative discharge of tax liability while filing return of output tax through electronic cash ledger and it should be more than 1 per cent up to the month of filing return.

The taxpayer is also exempted from this rule if they are a government department, a Public Sector Undertaking (PSU), a local authority, or a statutory body. According to experts, this rule is mainly applicable to businesses with annual taxable turnover of more than Rs 6 crore.

In other words, the rule is applicable to businesses if their taxable turnover for each month in a year is over Rs 50 Lakh, are not engaged in export under Letter of understanding (LUT) or Inverted Supply, are a taxpayer itself or if its partners or directors are not paying Income Tax in excess of Rs 1 lakh, and has not paid at least 1 per cent of the cumulative total output liability up to a given month through cash ledger.

Sections of business communities impacted

In the opinion of CA community, the main idea behind implementing this rule is to discourage businesses that take fake credits. According to the amendment, the rule overrides all other rules. Though there is a threshold of Rs 50 lakh, the rule will be applicable to businesses such as service providers.

Presenting its review on Taxguru, CA Hitesh Patel, a partner at Mehta Patel & Co from Ahmedabad elaborates about the businesses that will be directly impacted under this rule. He says, “In my honest opinion, not many taxpayers would fall under this category as they would ideally be discharging 1 per cent or more of their output liability by cash ledger.”

He further mentions, “Taxpayers covered under this category would ideally be engaged in any seasonal commodity business, business of contractors where running invoices are issued, and businesses where instance of levy arises very few times in a year such as CAs who issue tax invoices in September or October after completing service of audit or other filings and annual maintenance contracts business etc.”

Paying output tax liability through cash every month is going to be burdensome for various businesses. Experts also recommend businesses to keep some extra cash in reserve for taxes since this can also result in capital crunch for operating businesses. To avail discounts, many businesses stock products and then sell it gradually. When the product is seasonal, firms will have to carry forward ITC and will have to make the payment in cash.

Patel also points out that the rule is going to hit some genuine taxpayers falling under specified criteria. He further explains that this particularly includes a business which has incurred huge capital expenditure resulting in large ITC on capital assets and business loss due to depreciation claim on capital expenditures. In another condition the rule is applicable, if a taxpayer has brought forward huge loss under income tax and has genuinely availed ITC credit.

Prevention of fraudulent activities through the rule

The GST evasion and generating fake invoices has inadvertently become a racket nationwide. These frauds impact cash flows of government and also siphon off GST refunds. According to an estimate, the rule will be applicable to less than 0.5 per cent of total taxpayer base of 1.2 crore.

EY Tax partner Abhishek Jain says, “With the government providing reasonable exceptions to this rule, the idea remains to prevent misutilisation of credit by businesses that take fake credits. Government has also restricted filing of outward supply details in GSTR 1 return for businesses who have not paid tax for the past periods by filing GSTR 3B. The idea here seems to curb input tax credit passing by businesses which have otherwise not paid their GST liability.”

According to other tax experts, those asserting for huge sums in fraudulent ITC will be in jeopardy since now they will be forced to pay cash that may amount to crores now. In other words, the rule will help to identify where the risk to revenue is high and where it will deter the fraudsters who are running a multi-layered scam of fake invoices. Adding to it, it will then pinpoint GST scammers with zero financial credibility showing high turnovers, misusing ITC, issuing fake invoices, and fleeing.

On the contrary, an analysis by Nexdigm, a tax consulting and accounting services firm states that government is attempting to find out means to identify fraudsters through this amendment. “However, excluding taxpayers where people controlling the organisation are discharging income tax perhaps show that some data analytics is at play. Therefore, it is likely that some of the honest taxpayers like those making losses due to pandemic may be hit by this change,” says the paper.

Discussing the same in a webinar, Sanjay Aggarwal, President, PHD Chamber mentioned that there have been many instances of frauds due to fake invoicing since the implementation of GST. There is a need to improve the system as well as the administration to check frauds.

He felt that the seamless flow of input tax credit forms the backbone of GST, and any form of restriction on the ITC will be a dampener for the spirit of GST. “Any form of amendments should promote voluntary tax compliance, reduce tax litigation, and benefit taxpayers by providing them peace of mind, certainty, and savings on account of time and resources that would otherwise be spent on the long-drawn and vexatious litigation process.”

In another argument an expert commented on anonymity, “Since it is a beginning of the financial year, adhering with the rule will be daunting for genuine and big taxpayers. It will also be a challenge for various account professionals to answer their clients and filing tax at the same time.”

He also feels that the government step has come at a time when businesses are already struggling. He further adds, “The announcement has created an air of confusion as well as a negative sentiment among businesses. Imposing stringent laws depicts that government lacks trust on the taxpayers. It may somehow impact on the government’s initiatives and goal towards making India self-reliant.”

Extent of impact on small firms

Discussions on whether the compliance of the rule will affect the ease of doing business or will impact small and medium businesses are widespread. The general conception is that mandatory cash deposit norm will be hefty for businesses. But, it is necessary to understand that the compliance is on liable tax and not on the monthly turnover.

In fact, if calculated it amounts to only 0.01 per cent of the turnover. For example, if a trader sells products worth Rs 1 crore on which tax rate is 12 per cent and if he is discharging his tax liability more than 99 per cent through ITC, then he has to pay only Rs 12,000 under this rule. On the other hand, a composition dealer would have to pay Rs 1 lakh in cash with this volume of sales.

CBIC in a tweet also clarifies that the rules will not impact small businesses, because its compliance specifies a monthly turnover of Rs 50 lakh or more. There is no doubt that the genuine taxpayers still form a majority in Indian tax system. But the intent to unearth frauds and GST scams may result in creating unnecessary hassles for genuine taxpayers. Therefore, businesses are apprehensive of it and are approaching tax authorities for more clarity.