It’s official: Cryptos and other similar digital assets are to be taxed at 30 per cent. The announcement has caused a commotion in the market, with speculations galore doing the rounds about India legalising cryptocurrency.

And we use the word ‘speculations’ because the government’s stance about whether they simply made it legal is still unclear. Though, it is a tacit step from the government to bring the income generated through the sale or transfer of cryptos under the tax ambit.

But it raises a few questions as well. The first obviously about the legality of cryptocurrencies and the second about whether this announcement implies that there has been a change in the bill that was supposed to implement the prohibition of cryptocurrencies.

And of course, now people must be thinking about whether to invest in them or not.

“I am in two minds over the digital tax. On one hand, it shows a welcome tax-don’t-criminalise attitude. We need to broaden the basket of choices for people to invest their savings in. Nevertheless, 30 per cent for any tax only incentivises evasion,”

comments Sanjay Dangi a financial investor to many start-ups and Director at Authum Investment and Infrastructure Ltd.

If this is not confusing enough, another statement from finance secretary TV Somanathan just a day after the budget was unveiled has now engendered more contradictions on the proposal to tax virtual assets.

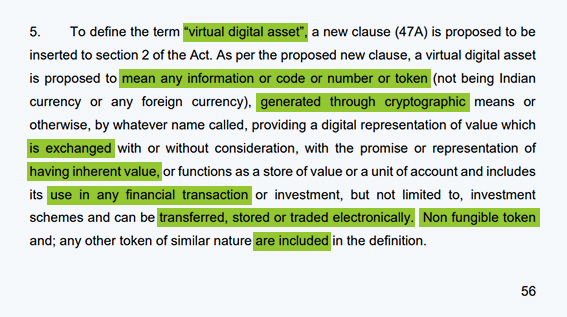

Here is the statement for your perusal.

So, to assume that cryptos are suddenly okay in India, is rather hasty. However, the new crypto tax regime in addition to the Digital Rupee is a watershed moment for India. At least, now we know the government’s stance on virtual assets.

What are virtual assets

We understand that bringing virtual assets (cryptocurrencies) into the tax ambit and announcing the Digital Rupee is big news. This gives us a sneak peek into the government’s preparations for India’s crypto future, in which these concepts will become mainstream.

First, noticeably the Finance Minister did not use the term cryptocurrency in her speech at all. Instead, she mentioned virtual digital assets—what are they, and why are we assuming that they refer to cryptocurrencies?

According to the clarification in the budget document, the government defines something as a virtual digital asset if it is generated through cryptographic means or otherwise, represents a value and can be stored or traded electronically.

Clearly that’s the textbook definition of cryptocurrency.

Now let’s take a look at how this industry is growing in India.

The crypto industry at a glance

Just a few years back or even until recently, crypto was just a fad. People probably did not imagine that it was going to become an industry one day. But it is here, and it is growing at a mindboggling rate.

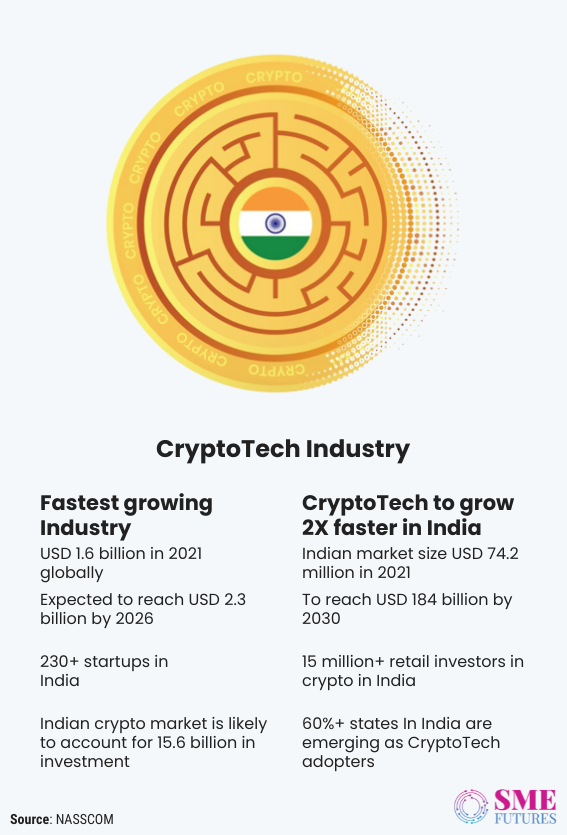

NASSCOM says that there are over 230 cryptotech start-ups in India. As India’s cryptotech market started to pick up, it stood at US$ 74.2 million in FY2021, a growth of 39 per cent in the last five years.

Meanwhile, with the evolution of crypto, the country is witnessing the rise of a new class of investors, the launch of various NFTs and their usage in various industries. Industry estimates suggest that there are 15 to 20 million crypto investors in India, with total crypto holdings of around 400 billion rupees ($5.37 billion).

Given that the cryptotech industry value chain can now be used in a variety of industries, it will have its hands full in addressing the emerging challenges in a variety of industries.

A win for the crypto industry

The recent news about cryptocurrencies and NFTs has generated a positive buzz among elated crypto enthusiasts. Since the tax has always been applicable to gains on virtual digital currencies, the ecosystem lacked clarity on the subject. Now there is a unanimous sense of excitement among the crypto industry’s players.

“No expenditure deduction except the cost of acquisition. It’s a win-win situation! Now, retail investors should no longer worry about whether they can invest in cryptos or not,” says Bibin Babu, Co-founder at MetaSpace, a play-to-earn NFT game platform.

Mo. Akram, Ideator at MetaSpace says, “Remember, the government has come a long way in its stance towards crypto as was seen in the last Union Budget. This, I feel, is a step in the right direction to usher in a new era of innovation in India, which will help it to grow digitally as well as economically.”

On a similar note, Avinash Shekhar, CEO of ZebPay feels that this decision will herald a new era of growth and innovation for India in a Web 3.0 world. “The move to tax virtual digital assets gives the entire ecosystem including the investors and the exchanges transparency on the road ahead. It hints at an optimistic sentiment towards the further acceptance of cryptos and NFTs across the stakeholders in the country,” he says.

“Cryptocurrencies coming into the tax ambit, puts an end to all the speculation and confusion. The 1 per cent TDS is a master stroke for also tracking the trading volumes and monitoring the movement of liquidity through cryptocurrency exchanges,” says Dr. Gunjan Bhardwaj, Founder and CEO of Innoplexus.

Ashish Singhal who is the Founder and CEO of CoinSwitch and Co-chair at the Blockchain and Crypto Assets Council (BACC) says that the budget shows the government’s intent to take a business-friendly approach while protecting the interests of the consumers and the exchequer.

“Regulatory guidance on tax not only furthers the mainstreaming of this emerging asset class, but it is also the gateway to the future decentralised world, aka Web 3.0. We hope to work with the government to help bring crypto-asset taxation at par with other asset classes and participate in the central government’s vision to promote economic growth,” he avers.

Chipping in with his views, Abhay Aggarwal, Founder & CEO, Colexion believes that the move will provide a base for monitoring, authenticating and regulating the crypto ecosystem in the country and for bringing transformations in it when required.

Recognition = legality?

Players like MetaSpace, ZebPay, and others believe that this step legitimises cryptocurrency. However, given the finance secretary’s statement that India will not make crypto assets legal tender, others believe that it is best to wait and watch for the time being.

“The government seems to be approaching the crypto space with a comprehensive understanding, while keeping in mind the P2P nature of crypto,” opines Roshan Alam, Co-founder and CEO at GoSats. “While we eagerly wait for the crypto bill, we expect positive and well-thought regulations going ahead, which are strongly needed for consumer protection. UPI and Aadhar are ground-breaking and world-renowned finance and governance initiatives. We hope for the same from the Indian crypto regulations as well,” he further elaborates.

Another player, Vikram Tanna, COO, Mzaalo also feels that it is better to wait until the rollout begins, “The move brings the much-needed clarity on how the government views cryptocurrencies and should eliminate any fear that the user/investor class might have had around the cryptocurrency ban. We now await more clarity towards the rollout of these measures in the upcoming days,” he comments.

So far around the world, El Salvador is the only country to adopt Bitcoin as legal tender.

This decision will also engender the add on process of tax filing for the crypto based companies. Which implies that there will be more work for these firms. The crypto exchange operators in India are seeking more time to get ready for this.

One such player Vikram Subburaj, CEO, Giottus Crypto Exchange says, “We await the details on what is a taxable event and what is the threshold for 1 per cent TDS deduction. We do hope that the government will give the exchanges and the other businesses a certain time period to enable the tech behind TDS deduction and bookkeeping. Offsetting and carry forwarding losses have worked well in other countries but we are happy to see that consideration is being given to all such instances.”

30 per cent is way too high

Digital assets are now in the highest tax band. Furthermore, the majority of stakeholders are in agreement about the fact that a 30 per cent tax rate is excessive.

Tax consultants reckon that individuals could end up paying more than 30 per cent of their crypto profits in tax and other charges.

“If you made a profit of 100 rupees, then including the 30 per cent tax bracket, plus surcharge and cess, the total tax outgo will be around 42 rupees,” explains Amit Maheshwari, Partner at AKM Global, a tax and consulting firm to Reuters.

Venus Dhuria, Co-founder, AppyHigh, a mobile internet consumer technology says, “The benefit of recognising anything via regulation is that it prevents unscrupulous or illegal activities in the space. But a 30 per cent tax rate is on the higher side, and more clarity is required on the setting off of losses. However, this is still a start and hopefully with time more clarity will emerge.”

Others think that this might discourage the new investors, particularly the younger people as they are more prone to crypto investing. “Taxing income from digital assets at 30 per cent may discourage some investors as prima facie it appears severe,” feels Pratik Gauri, Co-founder, and CEO of 5ire, a first level 1 blockchain technology player.

#ReduceCryptoTax was trending after crypto enthusiasts started expressing their views about a reconsideration on the 30 per cent tax slab.

In an attempt to get this crypto tax reduced, the crypto stakeholders are organising petitions and campaigns on Twitter urging the government to reconsider the tax.

What kind of impact will this have on NFTs?

NFTs or non-fungible tokens are becoming increasingly popular and are growing exponentially.

Blockchain data company Chainalysis estimates that the NFT market will be valued at $41 billion by the end of 2021. Many celebrities too have adopted the technology and have launched their own NFTs worth millions and billions of dollars.

Because NFTs are lumped along with cryptos as virtual assets in the same bracket, it implies that all type of NFTs or the virtual experiences purchased on metaverse will come into the tax ambit. However, worldwide NFTs are still classified as non-taxable assets.

But not in India, not anymore.

Keyur Patel, Co-Founder and Chairman of GuardianLink and BeyondLife.Club says that the government should allow the industries like gaming, Interactive Immersive museums and other edutainment NFT frameworks to succeed without having to shoulder a tax burden.

He says that these asset classes being treated differently creates a one-sided tax implication versus defining cryptos as a Traceable Asset and NFTs or Gaming Virtual Goods as Entertainment / Collectible Assets. Like Digital Music or Digital Art.

“It is version 1.0 of the framework. We understand that regulations are required to control the other elements of crypto. NFTs are at nascent stage and with such taxation, will have to eventually adjust for the growth of the developing ecosystem,” he says.

As NFTs are still classified as non-taxable assets worldwide, for future amendments, Patel recommends that the government should consider the fact that a crypto token and an NFT token are very different from each other.

Further commenting on how the NFT space will be impacted due to taxation, Patel says, “For cryptos, no deduction other than the cost of acquisition should be allowed and no set off should be permitted against other incomes or losses. Also, tax withholding should be triggered on a sale at 1 per cent beyond a certain threshold. This implies huge friction initially until the user base understands that all asset classed must be taxed for holistic economic growth. Initially, this will create a major roadblock for the investor community.”

The new tax proposition will take effect from 1st April 2023, for the assessment year 2023-24.

On the whole, the government’s stance on cryptos is now being perceived optimistically, with many forecasting that this decision will usher in more innovations and spur India’s economic and digital growth. However, given the nascent stage of this industry in India, the players are of the opinion that the centre should take a relook at its proposed tax structure for this industry and should reconsider its implementation as well.