The last two years have been among the wildest in real estate history, with the COVID-19 pandemic hastening the recent trends.

A new era of online home buying and selling has taken off. Low stamp duty and interest rates in recent quarters have boosted the sector, increased demand and boosted the confidence of the homebuyers’ as well. The recent volatility in the stock market, as well as the currency benefit of the rupee-dollar exchange rate, have made it attractive for NRIs to invest in real estate in India.

Soon after the vaccination drives began, the industry began to grow in terms of new and improved launches in response to market demands and financial inflation for the sector’s benefit.

On top of all that, heavy returns, good rentals and improving infrastructure have been the additional key drivers.

At the same time, consumers too recognised the importance of owning a home, thus, driving up demand. They are looking for more room for themselves. Location, connectivity, and amenities are becoming the critical deciding factors for them. Homes located in societies with better health and security facilities are taking precedence. Commercial properties too have enhanced their technology factor and have changed as per the new standards.

Real estate experts have seen 2021 as a period of rapid transformation. Developers too have invested in technology and digital channels to reach out to consumers in a more efficient way.

As we move into the new financial year, the experts read the tea leaves and predict an optimistic 2022 for the real estate industry.

The residential property market is on a strong footing

After a prolonged period of falling and then stabilising, residential property prices are likely to start rising again. A Knight Frank 2022 report projects around 5 per cent capital value growth for the residential property segment in the country in 2022.

Many of the supply and demand-side factors, assessed over the last decade, have started putting an upward pressure on house prices. This momentum is expected to continue in 2022 as prospective homebuyers’ preferences for bigger homes, better amenities and attractive pricing will keep them interested in sealing the deals.

“Demand in residential sales would remain there,” says Pritam Chivukula, Co-founder & Director, Tridhaatu Realty and Hon. Secretary, CREDAI MCHI. “Well-known and trusted developers shall be witnessing comparatively better sales in the mid-income and affordable housing segments and shall continue to dominate in 2022 as well,” he says.

Rajat Rastogi, Executive Director, Runwal Group, also expects the demand to remain robust, “Especially in the affordable housing segment and in the ready to move in or soon to be ready projects,” he says.

“As a group, we have seen a significant increase in revenues consistently and we expect the same trend to continue in 2022. We have a positive outlook and new launches, deliveries and further expansions are in the pipeline for the coming year,” he adds.

The demand will be there on the back of the change in consumer behaviour mostly. Owning a home is no more a matter of investment preference, but a necessity, given the boost that a luxury residence is meant to provide in the wider perspective of work-life choices.

This has given a boost to luxury homes sales, says Shraddha Kedia-Agarwal, Director, Transcon Developers. “There is a shift in demand for sea-facing homes with large open spaces like balconies, terraces, courtyards, gardens, and parks in the vicinity. The WFH culture has changed the pattern for most home buyers. The shift of customer preferences from premium to a more sophisticated approach, is expected to continue this year as well. Buyers want to get a lifestyle that can flawlessly include the WFH notion, while not giving up on the lavishness and comforts of luxury living,” she comments.

Foreign investment will drive this sector

Foreign Direct Investments (FDI) remain an important growth driver, and the same applies in the case of the real estate players as well.

Commenting on the sector’s performance in this regard, Kedia feels that Indian real estate has succeeded in attracting foreign moolah, especially in the residential market.

“The residential real estate market in India has become more lucrative for ultra-high net-worth individuals (UHNIs) and NRIs as a result of the increased transparency and ease in investment norms,” Kedia says.

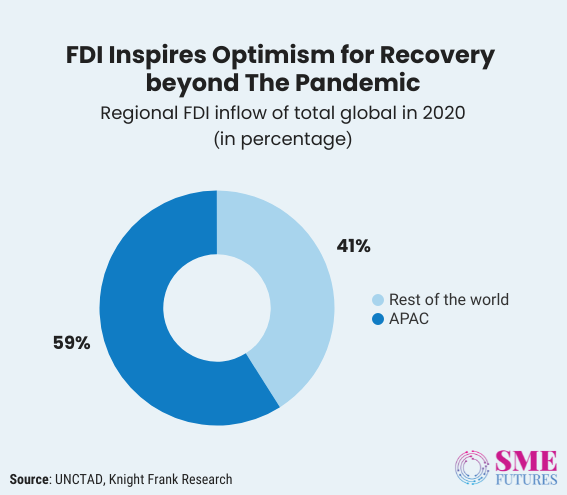

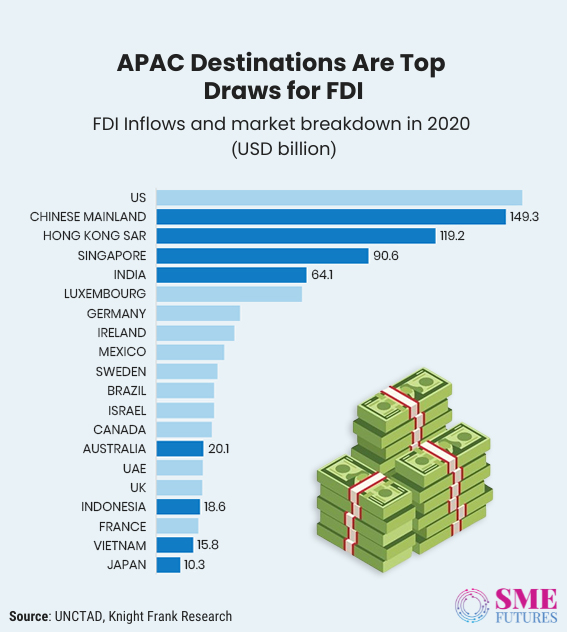

With RERA ensuring transparency and laws allowing 100 per cent FDI in construction, Indian real estate is witnessing sharp investment infusions from NRIs. The Knight Frank analysis also speaks the same language.

The analysis shows that the APAC nations including India continue to be an attractive investment destination, as evidenced by the FDI strength in this region.

Of the top 20 investment destinations globally, the Asia-Pacific economies come in at number 8. The Chinese Mainland remains the most attractive destination for FDI, accounting for 9 per cent of the total FDI volume globally. Meanwhile, India also continues to attract higher levels of FDI. See for yourself.

“The new class of ultra-rich people is on a buying spree of luxury homes in global cities like Mumbai, Bangalore, etc. With a huge part of the vulnerable population already vaccinated, the Indian markets are proving their grit and potential and it is now time for investors to decide if they want to benefit from India’s future potential,” Kedia asserts.

Property prices will go up

1.38 lakh housing units were sold in 2020. When compared to the previous peak in 2014, this was a rock bottom of 60 per cent. However, between January and September of 2021, 1.45 lakh units were sold. This was a 5 per cent increase over the sales in 2020.

Undoubtedly, there are a fair share of reasons behind this demand.

As a result, 2021 saw good traction in the mid segment (units priced between Rs 40 – 80 lakh) and high-end (units priced between Rs 80 lakh – Rs 1.5 crore) categories. Altogether, around 65 per cent of the supply between Jan – Sep 2021 came in these segments.

Anarock property consultant’s consumer survey shows that there was a clear rise in the preference for properties priced over Rs 90 Lakhs. During the first wave, 27 per cent of the respondents preferred properties priced over Rs 90 Lakhs, which increased to 38 per cent during the second wave.

However, property values surged during the first year of the pandemic, on the back of various add-on inputs due to the new normal and the enhanced tech interventions. This implies that home prices will continue to rise, making it a bit difficult for prospective home buyers.

Anarock projects that new supply and sales might reach 2019 levels by the next year i.e., 2022. Interest rates may start inching up from the H2 of 2022. Prices may appreciate in the range of 5-10 per cent.

Given the statistics, Rastogi of Runwal Group agrees that this trend is here to stay. “We expect demand to remain robust, especially in the affordable housing segment and in the ready to move in or soon to be ready projects. Prices will firm up owing to the rising input costs as at some point developers will have to stop absorbing the further increase in input costs. Keeping aside the threat posed by the new variant, the real estate sector should see a great 2022,” he elaborates.

Co-working spaces will receive a piece of the pie as well

Businesses want to remain flexible on cost components in the face of a resurgence of COVID-19 caseloads. This has provided a brilliant opportunity for co-working spaces to suck up revenue from the agility-demanding businesses.

This, among other factors, will potentially double the market size of co-working spaces over the next five years at a CAGR of 15 per cent, reveals the latest CII-ANAROCK report ‘Workplaces of the Future.’

According to the report, currently, approximately 35 Mn sq. ft. of flexible office stock is available across the country. Of this, around 71 per cent or 25 Mn sq. ft. is by the large operators. Approximately 3.7 lakh flexi seats are currently spread across the major Tier I and Tier II cities of India.

Seen as a great option for cost saving, the idea of flexible workspace feels justified to most firms, mostly start-ups and they are taking it seriously.

“India is at the cusp of a coworking revolution with several large players operating across the country. Not just the existing coworking players but the new operators too have major future expansion plans. For instance, coworking player Smartworks is planning an approx. 20 Mn sq. ft. of coworking space comprising approx. 2.5 lakh seats over the next 3-4 years,” says the Anarock report.

The rapid expansion plans by these major coworking players, and the pandemic-triggered need to re-strategise workspaces, foreshadows a bright future for this new asset class. Companies returning to offices will have to consider leveraging flexi spaces to reduce cost and expenditure, and this will boost the demand for such spaces.

Some of the other notable key trends highlight that the warehousing sector will grow as e-commerce gains ground. The transactions of this sector are projected to grow at a compound annual growth of 20 per cent in FY 2023. The e-commerce part in the total warehousing transactions will increase to 36 per cent in FY 2023.

In this scenario, speed and technology will emerge as key considerations for the owners’ warehousing strategies.

Expectations from the government

The real estate industry has always been a dominant player and has contributed greatly to the country’s economic prosperity. In the coming months, the expectations of the buyers and developers ought to rise as the sector has been the recipient of a lot of newly formulated government policies.

Industry sources feel that these policies will help the industry to become more organised and will provide a boost to both the residential as well as commercial real estate segments. However, there are certain areas in which they require more handholding from the authorities in.

Pointing out those grey areas, Navin Makhija, Managing Director at Wadhwa Group says, “We need local authorities and departments like CFO/HRC/MCGM to create a Single Window System for approvals. These initiatives will help to bring down the cost of projects and ensure timely delivery which in turn would be beneficial for the buyers and meet the actual objective of RERA,” he tells us.

Adding to the list of wishes, Chivukula anticipates more incentives and extensions in relaxations for a better 2022. “Incentives like the introduction of tax benefits will help in increasing public spending with less transaction costs. Various supply and demand patterns assessed over the last decade have already started putting upward pressure on residential property prices,” he says.

Makhija agrees with this, saying, “We anticipate the government to announce incentives such as tax breaks which will increase public spending and lower transaction costs, etc.”

Going forward, the experts strongly recommend the real estate developers to focus on completing their existing projects. Which will eventually trigger sales given that the demand is there, and the buyers are more likely to go for the developed projects.

Meanwhile, the demand for luxury homes, affordable housing and ready-to-move-in homes will remain high. In addition to that, the players in this segment will witness relatively higher sales in 2022, as the various experts and the stakeholders of this sector are already predicting.