The International Monetary Fund (IMF), in its statement on March 5, 2022, stated that the war would have a significant adverse impact on the global economy, “especially on poor households from whom food and fuel are a higher proportion of expenses.” It also highlighted that “the sanctions on Russia will also have a substantial impact on the global economy and financial markets, with significant spillovers to other countries.”

The spillover impact on the Indian economy is already visible in form of Indian rupee’s depreciation, sale of equity by foreign portfolio investors, shifting of LIC’s IPO to the next fiscal, an increase in yield for government securities, and the central government’s recent decision to monitor its expenditure very closely.

Impact on India’s trade performance

Russia and Ukraine contribute only about 1 per cent to India’s exports and 2 per cent to the imports.

Russia is a bigger trade partner, with its share of imports being at 0.90 per cent and that of exports at about 1.5 per cent. Indian exports to Russia are relatively higher value-adding with chemicals, pharmaceutical and engineering exports constituting about 50 per cent of the total exports.

The composition of exports to Ukraine is not too different. If the trade supply chain continues to remain disrupted, Indian engineering, chemical and pharmaceutical firms would need to find alternative markets and prepare themselves for delayed flow of cash.

As for imports, petroleum, precious and semi-precious stones, vegetable oils and fertilizers constitute about two-third of India’s imports from Russia. On the other hand, nearly 80 per cent of Indian imports from Ukraine are for vegetable oils and fertilisers. As we know, India is dependence on imports of petroleum and vegetable oils is nearly absolute.

Since the war has led to a significant increase in crude oil and agricultural commodities, India’s import for these products would become very expensive. If the supply of these commodities continues to be disrupted, we can expect the domestic prices to go up. Combined with the depreciation in the value of Indian rupee, we may end up with a spike in inflation. Unless, of course, the government reduces import duties and/or domestic taxes.

Any reduction in duties is expected to reduce the fiscal space available with the government, compromising the government’s ability to support the economy. Given that the government has been reluctant to provide the required support even during the pandemic, the households and businesses would end up bearing the cost of this disruption too.

Spike in inflation: Impact on consumer and business

A spike in inflation, caused by commodity (metals and fuel) price inflation, is expected to have a cascading impact on prices of manufactured goods. If the prices remain at the elevated level for rest of the year, we expect the business to pass on these costs to the consumers.

While it is possible to beat inflation through growth in productivity in the normal course, it is impossible to raise productivity to beat the current level price increases that are more than 30 per cent across a range of commodities.

At the same time, the current spike in food and fuel prices is expected to adversely impact the household consumption and/or savings, particularly the low- and middle-income households. Given that an average employee has limited bargaining power, we don’t expect the wages to go up.

Consequently, it is expected that the households would bear the additional cost of inflation, which may either result in lower demand for manufactured goods and/or lower savings.

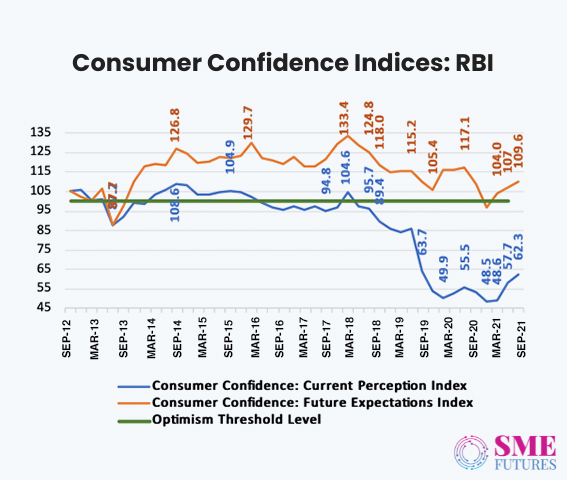

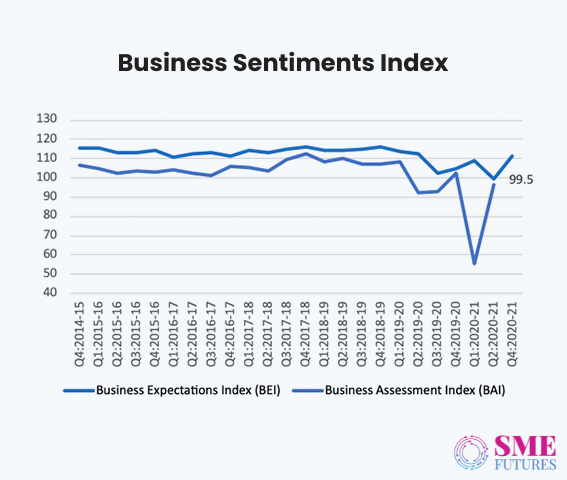

During the recent years, consumer as well as business confidence has been at a historically low level, as seen in the charts below, even before the conflict.

Impact on investments and flow of global risk capital

Private sector capital expenditure and global flow of risk capital are always very sensitive to conditions that cause uncertainty. For example, the COVID-19 outbreak led to large capital outflows from emerging markets, particularly by the foreign portfolio investors. The pandemic related outflows were “about four times larger than during the 2008 financial crisis.”

The current conflict has come at a time when the global economy has not even recovered from the economic collapse caused the pandemic. Global risk capital starts looking for safety and tends to move back to developed markets. If the conflict is not resolved quickly, we would expect a slowdown in flow of risk capital to emerging markets. While India is better placed than many smaller emerging markets, it would still need to find ways to attract global risk capital at this stage.

Production linked incentives schemes, currently being promoted, should help improve investment sentiment in the Indian context.

Cash flow disruptions and increased uncertainty

If the sanctions that restrict the flow of funds across the global system remain in place for many more months, the Indian businesses would have to be prepared for their cash flows being disrupted either because of delays in receipt from customers or the suppliers seeking advance payments or simply the delay in supply of goods. It would, therefore, be wise for an Indian business to negotiate contingent lines with their banks for meeting the cash flow deficit arising from these disruptions.